Opinion: Bornali Bhandari and Pawan Kadyan

The Covid-19 pandemic has brought public finances into the eye of the storm. Efficient and effective Public Financial Management (PFM) in the 21st century involves the usage of Financial Management Information Systems (FMIS).

The key objectives of PFM are—“to maintain a sustainable fiscal position effectively allocate resources and efficiently deliver public goods and services” (Cangiano Curristine and Lazare 2013). Diamond and Khemani (2005) define FMIS as a management tool that provides a wide range of both financial and non-financial information. It involves the computerisation of public expenditure management processes including budgets financial management of line ministries and other spending agencies.

The developments of FMISs in the country started in the last decade the technology of which was not available before that. The NCAER Direct Benefits Transfer Survey conducted in 2018 found that States were using two FMISs – one developed by the Centre namely the Public Financial Management System (PFMS) and their own State’s in-house FMIS.

Modern PFM comprises a set of complex processes rules and systems which are intrinsically linked with each other through the architecture of the FMIS. These architectures are being developed by different States and the Centre independently in a phase-wise manner. Consequently these FMISs are at different stages of maturity. The Centre is well-positioned to consider handholding States in developing their FMISs and interlinking the Centre & State level FMISs. Unlike Goods & Services Tax Network (GSTN) such interlinking should aim to maintain functional & data autonomy of State Governments which ensure their control over the developments in their own FMIS Systems ensure sufficient checks & balances to promote fiscal sustainability and minimise ‘float’ in the Systems. Interlinked yet independent Systems would lead to sustained capacity development in States and encourage higher innovations in PFM through healthy competition on one hand and promote fiscal federalism on the other. It would reduce the dependence on Bank Accounts to manage Public Finances. These systems could complement each other and systematically strengthen the exchange of learning between States and Centre.

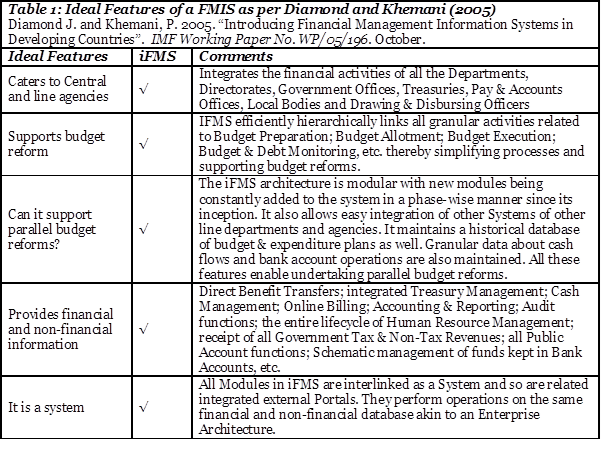

Amongst the State-level FMISs West Bengal (WB) is one of the more advanced ones. It is moving towards developing all features of an ideal FMIS as defined in literature (Table 1). The Integrated Financial Management System (iFMS) is a web-based application for streamlining the financial & fiscal management of the State Government.

Source: Authors’ conceptualisation from the literature.

Hashim and Piatti (2016) in their World Bank working paper titled “A Diagnostic Framework to Assess the Capacity of a Government’s Financial Management Information System as a Budget Management Tool” said that the effectiveness of the FMIS as a budget tool will depend on it having the following five features.

Treasury Single Account: It is a tool for consolidating and managing government resources. The iFMS has a web-based Centralised Treasury System. All Treasuries and their functions are integrated onto a unified architecture including Treasury functions like receipts payments pensions stamps PL Operations Deposit Accounts Provident Fund Monthly Accounts etc. Similarly the Bank Operations are linked into iFMS through Schematic Bank Account Management System (SBMS) Module.

FMIS coverage: All government transactions are covered by the iFMS (Table 1).

Online budget tool: The Centralised Budget Monitoring System a module within the iFMS has been developed for online submission of budget requirements by administrative departments and its processing at the Finance Department. Besides this the module has scope for an online integration with the RBI for obtaining the Clearance Memo for funds received from the Government of India through the Budget Route. The module also has provision for online submission of a request for creation of scheme head of accounts to Accountant General West Bengal thus reducing the time required for opening of any new subhead under any Head of Account. Further all Centrally Sponsored Central and State Schemes can be monitored online and utilisation of funds tracked on a real-time & actual basis.

Ancillary Features: It has all aspects of human resource management from appointment stage to pension stage of an employee’s lifecycle provides support for various auditing functions accords administrative approvals and financial sanctions links schematic bank accounts generates all kinds of role-based MIS Reports etc. The iFMS was also the first FMIS in the country to integrate with RBI’s e-Kuber Platform. It is also linked with the GSTN. A different platform iBudget exists for the preparation of State Budget and budget allotments of respective Departments which is integrated with the iFMS. Tools for managing fixed assets are being planned next in iFMS 2.0.

Technical Aspects: The entire IFMS is hosted in the State’s Data Centre (SDC) with its Disaster Recovery site at NDC. It runs its operations on a secure Multi-Protocol Label Switching network with West Bengal’s State Wide Area Network serving as backup. All the Treasuries are connected to the Central Server located at the SDC.

In sum there are alternative FMISs that exist at the State level which can be complementary to the PFMS. While the WB FMIS has the desirable properties & features and has proved its mettle during the pandemic detailed systematic impartial independent analysis can help States cross-learn from each other improve financial management and assess their effectiveness.

Bornali Bhandari is a Senior Fellow at NCAER and Pawan Kadyan is an IAS Officer belonging to the West Bengal cadre. Views are personal.