Opinion: Palash Baruah and DL Wankhar.

This is more so in rural areas. Insurance cover, public health are issues.

The Covid-19 pandemic has redefined our health policies and strategies. It laid bare the inter-linkages between the healthcare systems, its availability, adequacy and affordability.

At the core is the cost implication and impact on households over hospitalisations and healthcare interventions. The cost impact is most acute for those who bear it entirely out-of-pocket.

The worrisome and perhaps unsustainable aspect of healthcare financing is the rising out-of-pocket (OOP) expenditure for households. Per the December, 2023 study by the National Insurance Academy (NIA), over 50 per cent (in 2020) of healthcare expenses are borne directly by individuals. It signifies a substantial reliance on out-of-pocket payments.

So to finance their healthcare expenditure, people either have to dip into their savings or borrow. Not being able to easily finance their health expense would result in some section of the ailing population foregoing treatment, or resorting to desperate financing.

RURAL-URBAN DIVIDE

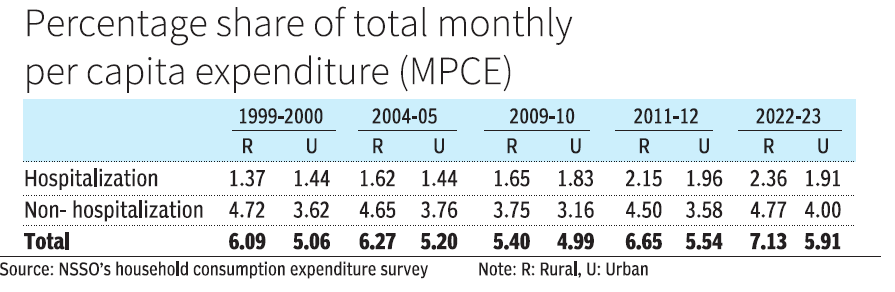

A close examination of the data from the National Sample Survey (NSS) rounds of household consumption expenditure survey spanning from 1999-2000 to 2022-2023 unveils an intriguing narrative.

Hospitalisation expenditure is showing a rising trend in rural households. Monthly per capita consumption expenditure (MPCE) on hospitalisation has risen from 1.37 per cent of the total in 1999-2000 to 2.36 per cent in 2022-23. In urban areas, the increase over this period is from 1.44 per cent to 1.91 per cent (see table). Lack of medical facilities and specialised manpower have forced people in rural areas to rush to urban and semi-urban centres and cities for medical treatment.

Hospitalisation expenditure is showing a rising trend in rural households. Monthly per capita consumption expenditure (MPCE) on hospitalisation has risen from 1.37 per cent of the total in 1999-2000 to 2.36 per cent in 2022-23. In urban areas, the increase over this period is from 1.44 per cent to 1.91 per cent (see table). Lack of medical facilities and specialised manpower have forced people in rural areas to rush to urban and semi-urban centres and cities for medical treatment.

Apart from the treatment and hospitalisation expenses, expenditure also has to be incurred on transportation, food and lodging. With better medical facilities, urban households’ share out of their MPCE in hospitalisation expenses is comparatively lower, except during 1999-2000, and it ranges between 1.44 per cent and 1.96 per cent.

It is also interesting that non-hospitalization expenses (i.e., OPD expenses on medicine, X-ray, ECG, pathological tests, doctor’s fees, and other medical expenses) consumed a much larger share of households’ MPCE in both rural and urban areas, with rural households being more disadvantaged.

Perhaps the frequency at which expenses are carried out for non-hospitalisation interventions is a factor. It hovered around 4.72 per cent in 1999-2000 to 4.77 per cent in 2022-23 with a slight dip in 2009-10 for rural households. It stood at 3.62 per cent in 1999-2000 and at 4.00 per cent in 2022-23, with a slight dip in 2009-10 in urban areas.

Cumulatively, it implies that rural households spent about 5 per cent to more than 7 per cent of their total monthly expenditure on hospitalization and non-hospitalisation expenses. It is lower for urban households at 5 per cent to less than 6 per cent of their monthly expenditure.

This variation could be explained by the fact that generally rural households have a lower per capita income and they have to incur travel expenses when they go to urban centres for treatment where medical facilities are better. The rising medical cost would further dent rural households’ budget.

Moreover, health insurance coverage in the rural areas is much less compared to urban areas. The NIA Report revealed that across age groups the “health protection gap” is in the range of 65-90 per cent in rural areas.

A VIABLE STRATEGY

Lowering the burden of medical expenses, especially out-of-pocket expenses, on households warrants a holistic approach for both the rural and urban households.

Public health spending in India has been abysmally low at below 3 per cent of the GDP. In the developed countries, it is between 6-10 per cent of the GDP.

There is a need to gradually raise it. Strengthening and supplementing the existing medical facilities and manpower in the rural areas will go a long way in reducing medical expenses.

Health insurance penetration in the country is not only inadequate but premiums have been on the rise. The government induced health insurance products through various schemes is limited in it reach.

According to the NITI Aayog Report of 2021, about 40.5 crore are the “missing middle” individuals who are not covered under any health insurance schemes. Insurance companies have so far been shying away to expand their coverage in rural areas.

IRDAI on May 10, 2024, issued a master circular directing insurance companies to do a certain percentage of business compulsorily towards meeting rural, social sector and motor third party obligations. Under this the general and health insurers would be allocated gram panchayat.

Every individual possesses a fundamental right to healthcare. Customised health insurance products along with improved public healthcare facilities will definitely contribute in lowering the burden of the households.

All stakeholders need to play a pro-active role. Any initiative aiming to reduce out-of-pocket expenditure is a step forward to prevent households from catastrophic healthcare expenditure.

Baruah is Associate Fellow at National Council of Applied Economic Research (NCAER); Wankhar is a retired govt officer. Views expressed are personal.