Opinion: Bornali Bhandari Samarth Gupta Ajaya K Sahu and KS Urs

Increased awareness and usage of government schemes may be partly responsible for the upswing in credit take among businesses in India.

Growth in non-food credit slowed down to single digits since 2019–20:Q2. In the NCAER Business Expectations Survey Round 116 conducted in March 2021 we had found t hat demand cost and non-monetary factors were responsible for low credit uptake by firms.

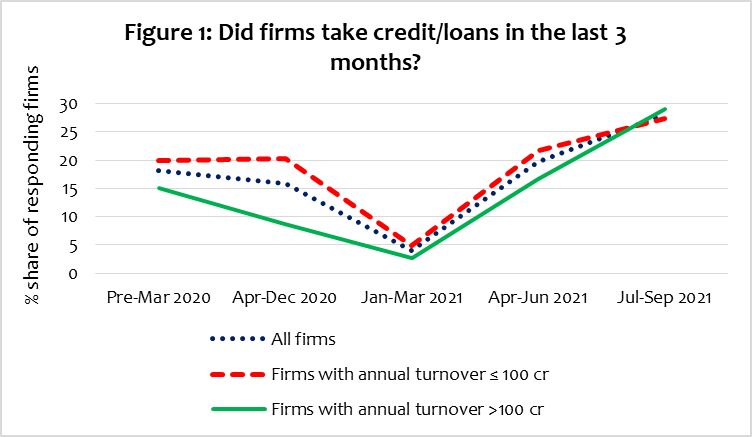

Credit uptake of firms has improved

However our recent explorations suggest that the situation of low credit uptake by firms may be changing. After troughing in March 2021 the NCAER BES Surveys conducted in June and September 2021 indicate that the share of firms taking credit has been going up (Figure 1).

The ‘large’ firms i.e. firms with annual turnover greater than Rs 100 crore are showing a sharper recovery.

Repeated surveys show that 80 per cent of firms take the the loans for working capital.

Sources: NCAER BES Rounds 116 117 and 118.

Awareness & Usage of Government Schemes for credit has improved

Increased awareness and usage of government schemes may be partly responsible for the upswing. In December 2020 nearly three-fourth firms were unaware of credit guarantee schemes.

This proportion fell down to only 5.9% in September 2021. Similarly the uptake of loans from Emergency Credit Line Guarantee Scheme increased to 13.4% in September 2021 from only 7.8% in March 2021.

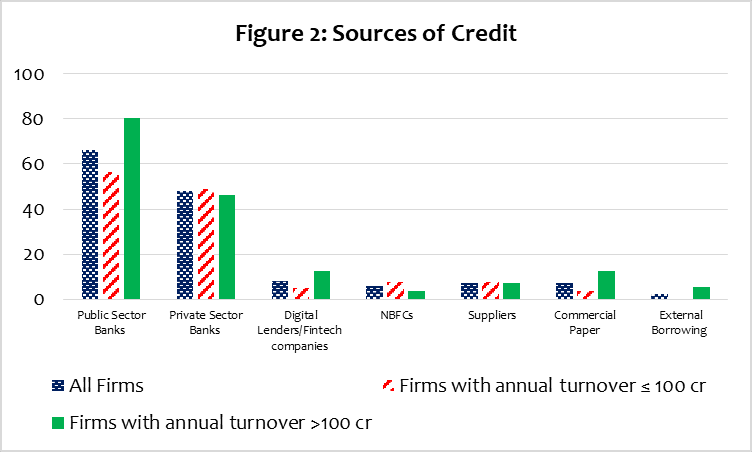

Sources of Credit

The next question is where are firms sourcing their credit. We find that 80 per cent of firms relied on public sector banks for their credit needs.

Interestingly 12.5 per cent of firms used digital lenders/fintech companies to avail credit. However we find that digital footprint varies by size and region. Neither firms with annual turnover ≤ Rs 10 crore nor firms in North and East used digital lenders for credit needs.

In contrast the NBFCs played a large role as a source of credit for small firms especially firms with annual turnover ≤ Rs 10 crore. Large firms additionally use commercial paper and external borrowing as other sources.

Source: NCAER BES Round 118.

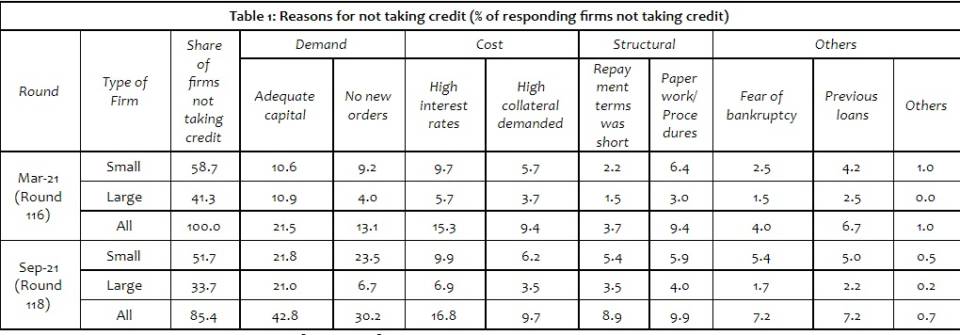

Firms are not taking loans due to demand factors

Table 1 compares firms which were not taking credit for March 2021 and September 2021 (we need to be careful about interpreting the results as in March 2021 we had asked firms for not taking credit for the last one year whereas in September 2021 we asked about last three months).

Broadly the results were similar across rounds that demand cost and structural factors played a role. Small firms were worse off in terms of ‘no new orders’ higher costs structural reasons and others.

However compared to March 2021 a higher proportion of firms were saying that they were not taking credit due to demand reasons.

Notably the share of smaller firms who were saying that they did not take credit because of ‘no new orders’ were 23.5 per cent in September 2021 compared to 9.2 per cent in March 2021. Further 42 per cent of firms viewed that they had adequate capital and so they did not take loan.

Source: NCAER BES Rounds 116 and 118.

Note: In March 2021 we had asked firms about reasons for not taking credit over the last one year. In September 2021 we had asked firms about the reasons for not taking credit over the last three months.

Policy Implications

Despite the improvement in credit uptake by firms the share of firms taking credit remains relatively low. Despite the presence of new players like NBFCs and digital lenders/fintech companies the role of banks especially public sector banks remains important. Digital lenders/fintech companies are not reaching the micro enterprises yet.

While the RBI Monetary Policy document in October 2021 recorded higher number of commercial papers being issued this year on a y-o-y basis the share of large firms using that as a source of credit remained low.

The main reason behind firms’ low uptake on credit in September 2021 were demand factors. Small firms were still not getting enough orders to take credit. This calls for better connecting firms especially small ones to internal and external markets via e-commerce trade routes connecting them to global value chains.

Bornali Bhandari is Senior Fellow KS Urs Associate Fellow and Ajaya K Sahu is Senior Research Analyst at NCAER. Samarth Gupta is a former Associate Fellow at NCAER. Views are personal.